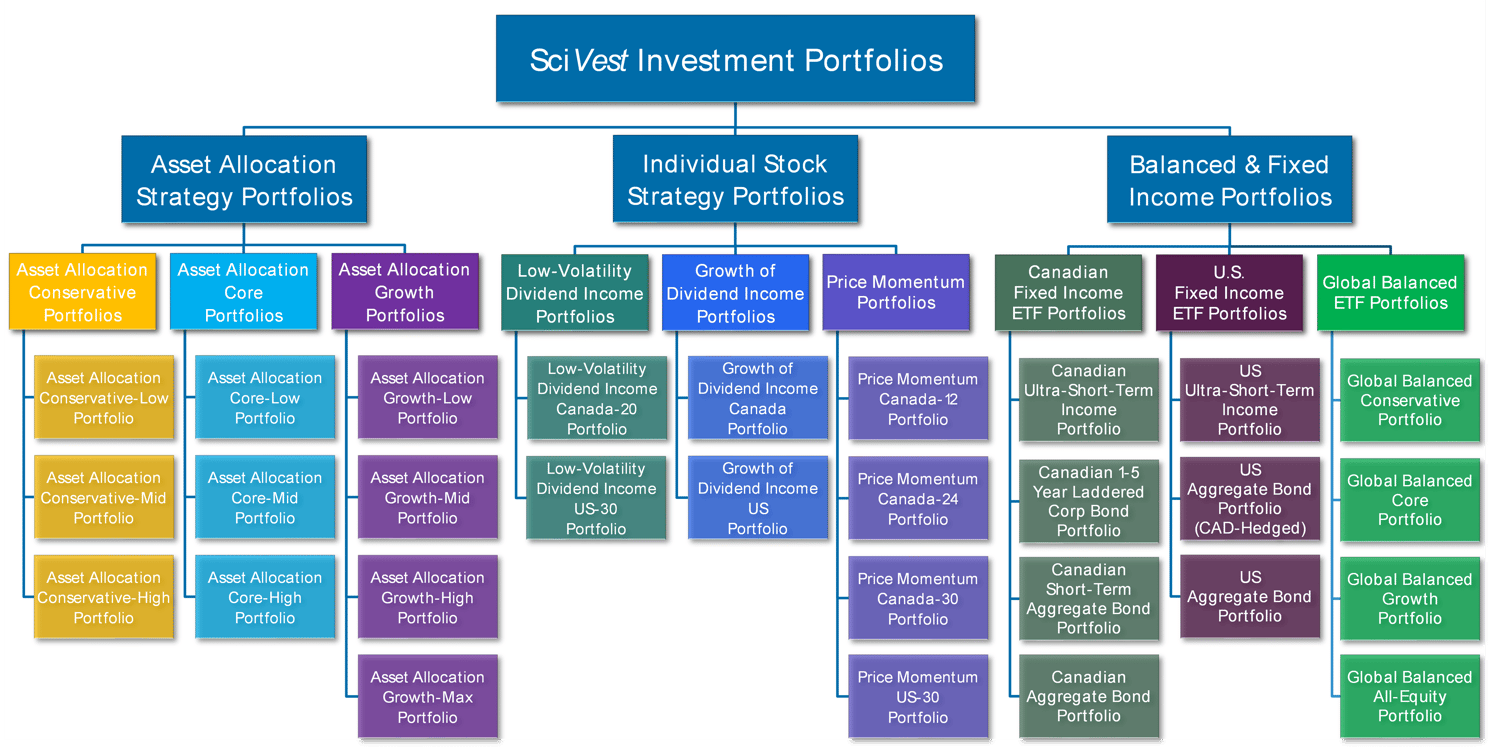

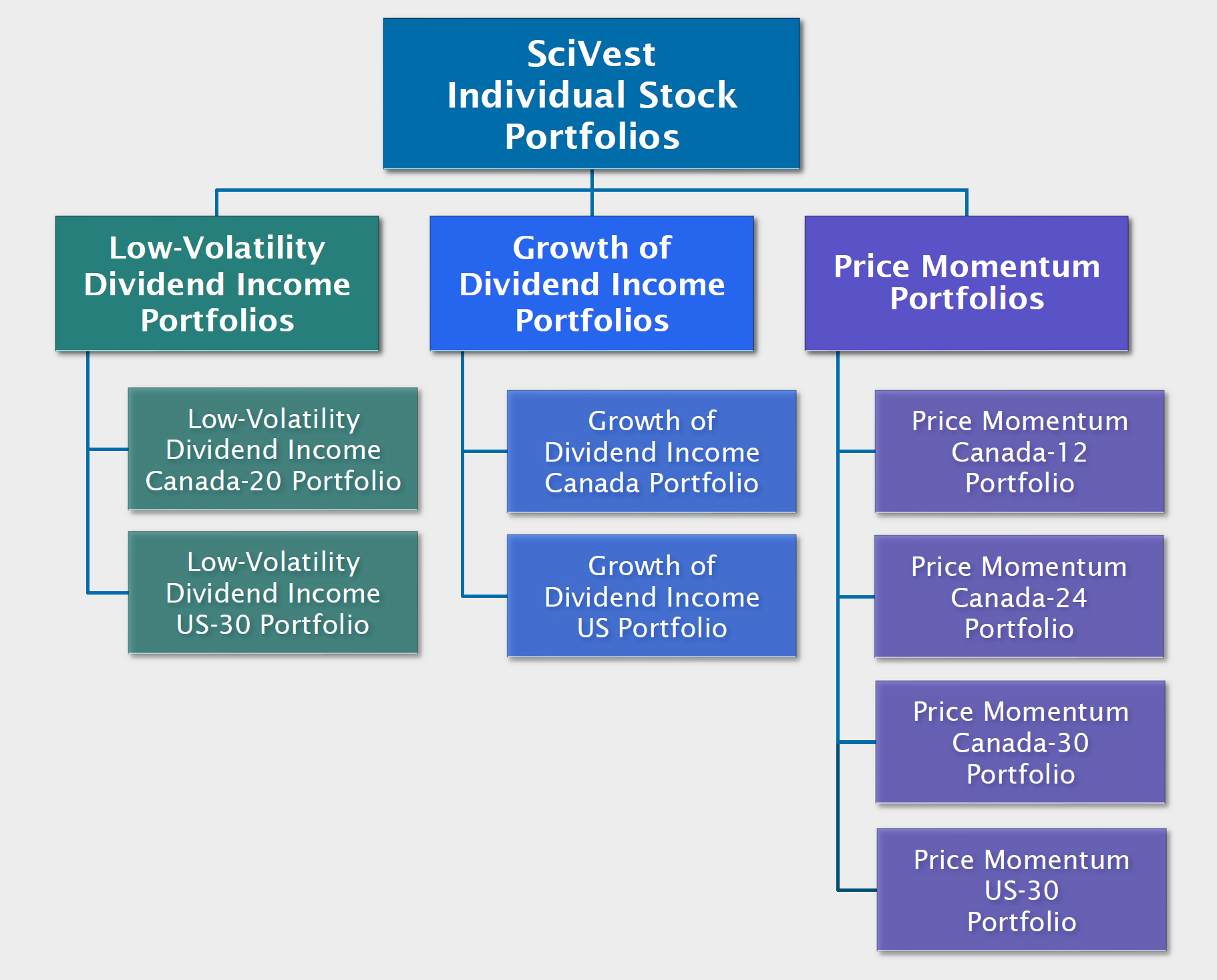

Individual Stock Portfolios

The addition of any of these "satellite" portfolios are terrific diversifiers and return/income enhancers to our SciVest Asset Allocation Portfolios, and therefore we encourage clients with large enough accounts to choose a combination of a SciVest Asset Allocation Portfolio and one or more SciVest Individual Stock Portfolio within each of the Accounts.

For a more detailed explanation of the individual strategies, please see the Investing tab, and review the Individual Stock Portfolios tab. Alternately, feel free to contact us directly for a more in-depth conversation on any of our strategies.